Upfronts Survey Indicates TV Spend Isn’t Going Anywhere

While we’ve been hearing a constant drumbeat of “recession” talk since last year, it may not have the presumed effect on the TV ad market – at least not for the 2023 Upfronts, anyway.

A recent survey from iSpot revealed 2023 upfront plans for over 500 brand and agency professionals, sharing insights around TV spending plans for 2023-24.

One of the big takeaways, right off the bat, is that 74% of respondents expected to spend at least as much as they did last year. Of those, 21% said they were planning to commit “a bit more” or “much more” than they did during the 2022 Upfronts.

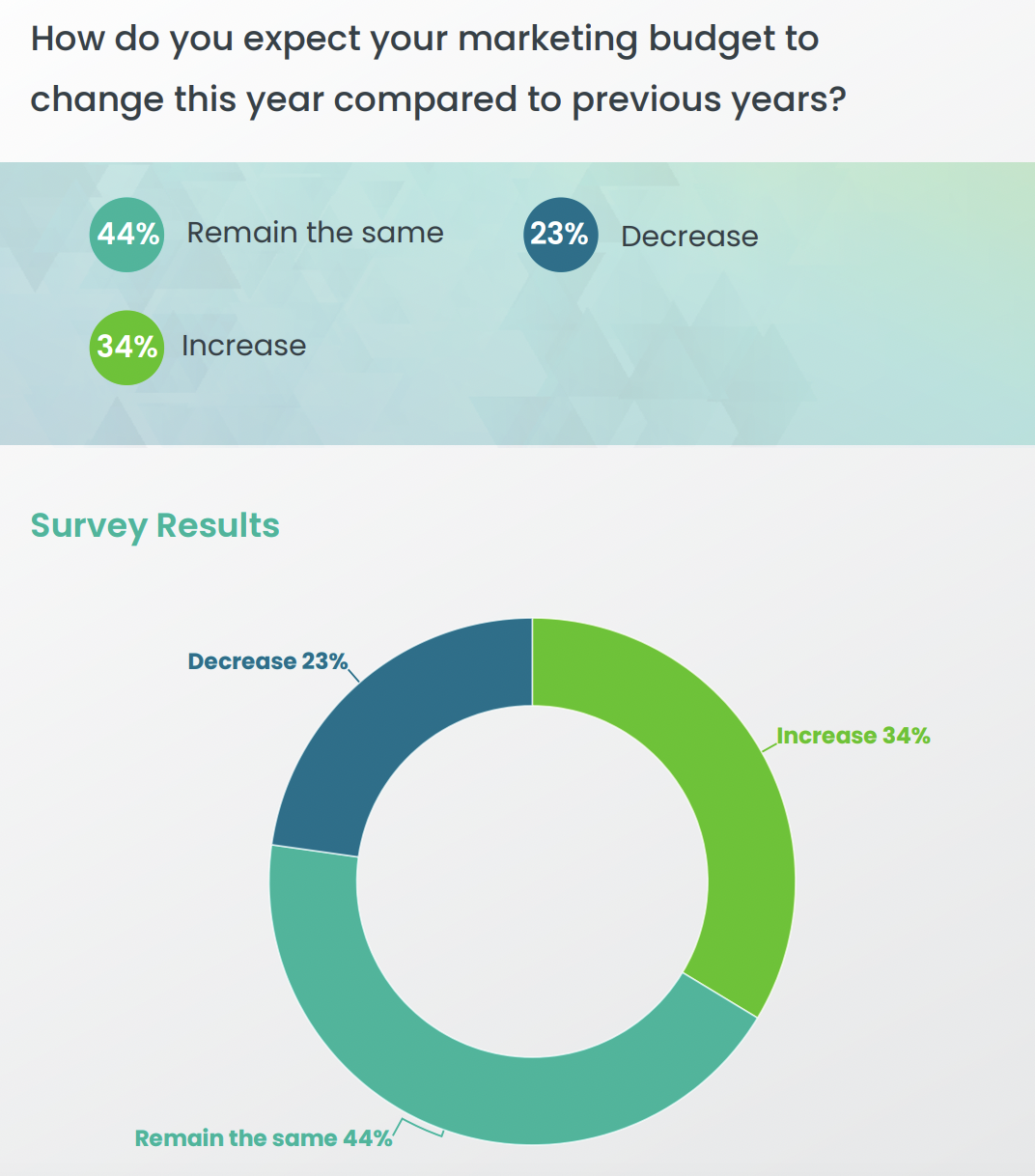

In conjunction with that, the survey also indicated that 78% still expected overall marketing budgets to increase (34%) or remain the same (44%), year-over-year.

While the results show that there’s definitely some hesitancy by brands and agencies to spend more in 2023, the fact that the overwhelming majority of those surveyed aren’t spending less seems to fly in the face of the gloom-and-doom we’ve been fed around the coming economic cliff everyone’s allegedly about to fall off. These things can change, of course. But ad buyers aren’t really incentivized to inflate their intentions here.

If spend isn’t going anywhere, then the coming upfronts should prove that TV continues to maintain its appeal, and if anything, looks even more valuable as a reach vehicle for a significant portion of buyers.

The results get even more interesting as you dig down further. Over 60% of respondents expected upfront commitments to be as flexible or less flexible than last year. Granted, a lot of that is dictated by who you’re buying ads from. But it does seem to indicate many brands are expecting a course-correction after networks were more amenable to their wants and needs in light of the pandemic.

Without the same threats of game cancellations, there’s understandably less of a need to be flexible when it comes to the biggest ad commitments (live sports). At the same time, though, with the looming writers strike, and ongoing questions for TV around residuals, special effects representation and more, more flexibility would still seem to be required.

Where that flexibility could already be built in, though, is in the form of unified buying interchangeably across linear and streaming programming – something that most of the major networks and their streamers have been doing in part and will seemingly continue to do.

Speaking of streaming, a lot of energy remains when it comes to investing with those services, and the measurement capabilities required to do so strategically.

Among those iSpot surveyed, 69% indicated they were very interested or somewhat interested in alternative (not Nielsen) currencies at this year’s upfronts. And 30% of respondents indicated at least a fifth of their upfront budgets will be allocated toward digital streaming platforms and nearly nine out of 10 respondents said at least 5% of budget would be utilized on streaming.

That’s a clear signal that a singular, legacy method of buying and audience measurement isn’t really enough anymore, and as streaming’s share of budget grows, the need for alternative currencies become even more pressing.

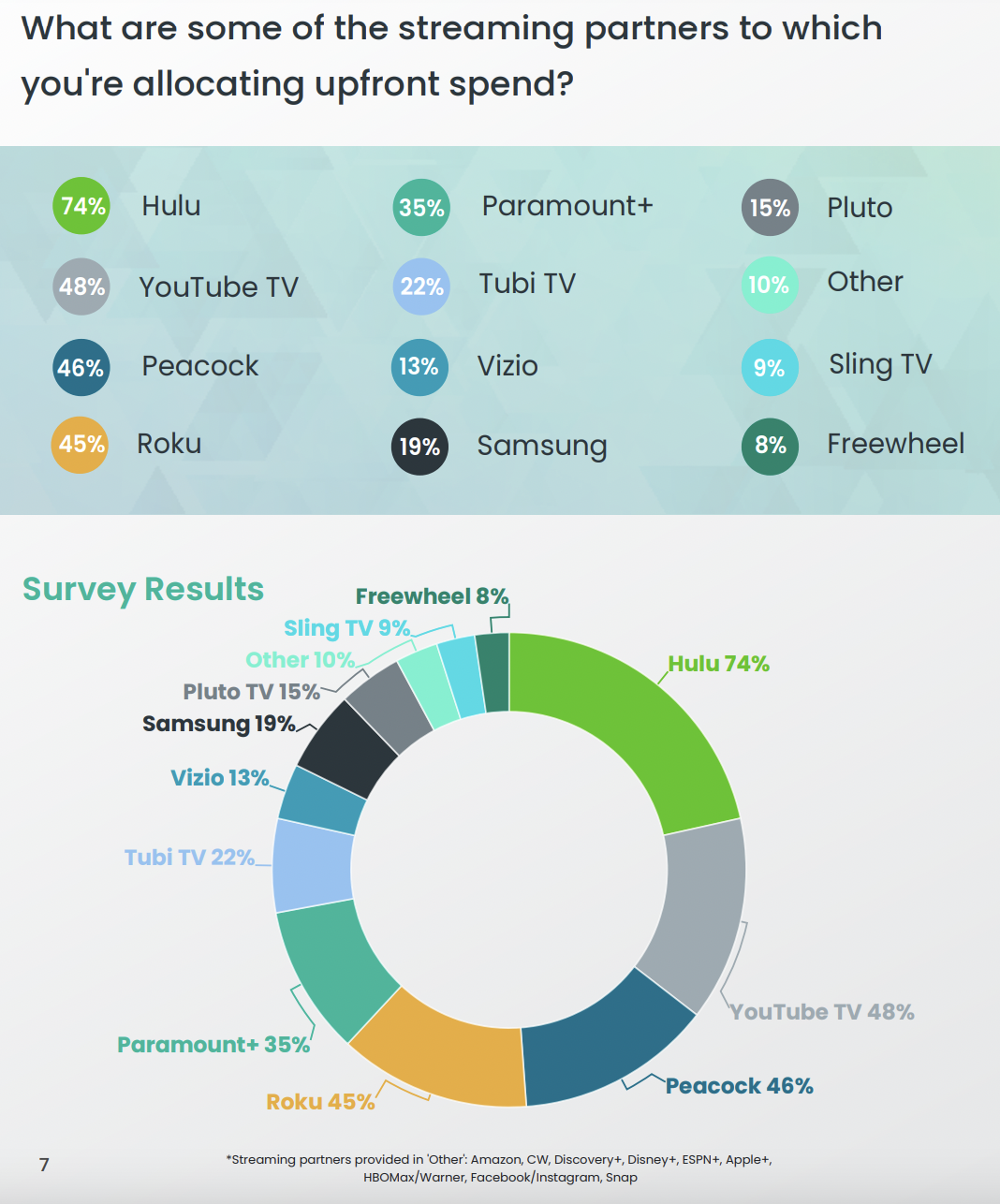

What’s also interesting is how much trust and business certain platforms already have. An impressive 74% of those that intended to spend on streaming were planning to do so (at least in part) with Hulu. That’s almost 30 percentage points higher than the nearest network-aligned streamer (Peacock, at 46%), which showcases just how much Hulu is ahead of competitors in terms of its ad product.

It’s a leadership position that’s minimally discussed when the rumor mill gets going every few months around what Disney does with Hulu next year. When Hulu’s this far ahead of competitors when it comes to buyer intent, and Disney’s looking to find additional ways to monetize streaming, what would possess the company to offload something so valuable to Comcast or Paramount?

Streaming is only going to grow, and that means Hulu’s position as a leader only gets more important over time. If Disney doesn’t keep Hulu in the fold, they’re punting away what could arguably be the most important part of the business a decade from now.

Check out the full streaming service rundown below, which also shows the potentially long road ahead for services like Netflix, Amazon and others, too.