Hot Takes: The 2023 Upfronts And Newfronts

The cherry trees here in New Jersey are in bloom and it’s still light out when I walk the dog at 7:00.

Which can mean only one thing: Upfront and Newfront season is just around the corner.

We asked our TVREV Thought Leaders Circle members to share their thoughts on what they’re expecting this year.

Perianne Grignon, VP Strategy at Mediaocean focused on two key trends: given fears over an uncertain economy, will advertisers spend money during the upfronts or will they hold back for now. And regardless of when they spend their dollars, advanced currency providers (ACPs) like iSpot and VideoAmp will play a huge role this year.

When it comes to what shape the Upfronts and Newfronts will take, the key word is “front” and how much advertisers are willing to secure in advance. Some buyers may read the market as being bearish and will opt for scatter and greater flexibility. Others may see it as an opportunity to lock in inventory for cost savings and share of voice.

Three big trends we’re focused on are audience, creative, and measurement. From an audience perspective, we’re enabling buyers to take a converged approach across linear and streaming video. With creative, we’re providing tools for personalization to increase relevancy and optimization. And for measurement, all eyes – no pun intended – are on advanced currency providers (ACPs).

With ACPs in Spectra and Prisma, Mediaocean customers will benefit from instant, tech-driven activation across all viewing devices, as well as advanced research reporting and discovery capabilities for more comprehensive measurement. Unlike traditional panel-based age and gender demographics, our platform enables brands and agencies to forecast and activate against custom strategic audiences, unlocking new possibilities for dominating the market.

Soon, planners and buyers within Mediaocean will have access to ACPs like VideoAmp and iSpot, in addition to Nielsen ONE and Comscore. This comprehensive approach will allow advertisers to create complete customer profiles using a vast array of valuable audience data, including viewing behaviors, spending tendencies, and demographic information based on location."

Tony Marlow, Chief Marketing Officer at LG Ad Solutions observed that the lines between the Upfronts and Newfronts were blurring as more and more consumers make the shift to streaming and advertisers follow suit.

The Upfront and Newfront marketplaces focus on brands investing heavily to find engaged audiences drawn to upcoming content opportunities. As the media landscape changes dramatically, CTV has become a vital tool for advertisers and brands to effectively connect with their target audiences on the largest screen at home. Recently, CTV adoption has skyrocketed, with more and more viewers cutting the cord and embracing streaming services for their entertainment fix, including those that support ads. As a result, advertising strategies for TV and video have shifted, causing the lines between Upfronts and Newfronts to blur, making the scene all the more exciting and dynamic.

Michael Scott, Head of Sales, Brand, North America, Samsung Ads looked at the impact of programmatic on advertising pre-sales, the impact of first-party data on buying decisions and the need to keep that data privacy-compliant.

For this year's Upfronts, here are the top three areas buyers are going to focus on: flexibility, working with partners who can provide solutions at scale, and leveraging first-party data in a consumer-first, privacy-compliant execution.

Media buying is now predominantly transacted programmatically, which certainly gives maximum flexibility to the buy-side. With the volume of quality impressions available in the streaming ecosystem, buyers no longer need to make firm commitments to set-aside scarce impressions. Buyers have learned that quality impressions are available, in great content with precision data that will drive outcomes. In the current economic climate, if cash is king, flexibility is its queen. Buyers are going to ask for more flexibility in media planning to evaluate spend and determine how they utilize advertising dollars on a case-by-case basis preserving budgets to maximize their impact.

Second, having a partner that is incredibly equipped with a wide spectrum of first-party proprietary consumer data will provide marketers with a significant advantage. At Samsung Ads, our rich first-party data and unmatched consumer insights enable advertisers to reach their target audiences with ad products that drive measurable impact and ultimately meaningful ROAS.

Lastly, advertisers get the biggest impact when they focus on their audience by leveraging their first-party data to reach consumers accurately when and where they’re watching content. With the rise of Data Clean Rooms and Privacy Enhancing Technologies, we enable our advertisers to bring their first-party data matched to our consumer data to drive scale and reach.

All the major content platforms will be sharing the latest content and talent at Newfronts/Upfronts, and Samsung Ads is slated to present on Tuesday, May 2. Our presentation will be featuring updates to our Samsung TV Plus service as consumers continue to fall in love with ad-supported platforms for their sophisticated user experience, premium content, and innovative ad formats. We expect a major theme during Newfronts to be legacy and newer streaming platforms alike turning to ad-supported business models to maintain growth. Rising tides lift all boats and new entrants to the AVOD marketplace reinforces the consumer demand for ad-supported streaming, and will bring more premium inventory into the market, to enhance the growth of the AVOD industry, which is good for all parties including buyers, sellers and consumers.

Evan Shapiro, media cartographer and CEO at EShap is focused on the ascendency of ROMI (Return On Marketing Investment) and why that means marketers will be pulling money from the upfronts and Newfronts and spending it on retail media.

CTV growth is plateauing. The NEW fastest growing segment of the ad economy is Retail Media. ROMI is the new CPM. This will be the first ‘Performance Upfront.’

After 2 years of skyrocketing growth, CTV revenue growth is plateauing. Advertisers will come back after a long pullback - but to what?

According to Advertiser Perceptions more than half of ad buyers are holding back budgets from the Upfront for scatter, and specifically for performance marketing: Return On Marketing Investment aka ROMI.

Of YouTube’s $29 bil in revenue, 70% is Performance Marketing - ROMI. As per Nielsen’s The Gauge, YouTube currently accounts for 9% of all CTV viewing. And that share will only increase.

54% of agencies/buyers say that ROMI is their top priority for the coming year.

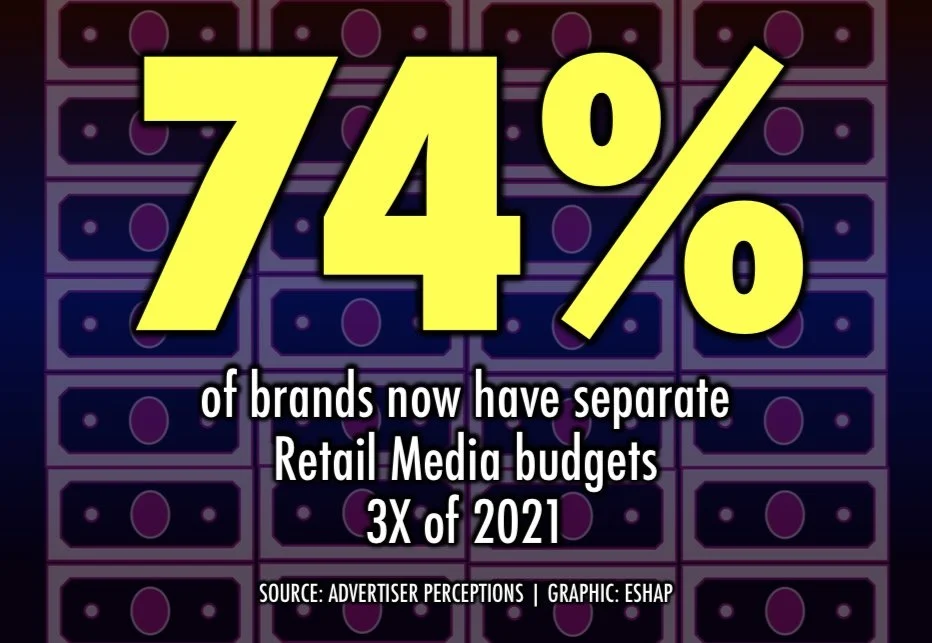

74% of brands now have dedicated Retail Media budgets. That’s 3X of 2021. Amazon did $37.7 billion in advertising last year - more than all of Paramount’s or Disco Bros revenues - in retail media.

Damian Pelliccione, co-founder and CEO, Revry, believes this year’s Newfronts will be better than ever for LGBTQ media as advertisers look to reach valuable audiences they have frequently overlooked in the past.

We are having a Newfront! Revry’s Newfront, the first ever LGBTQ-first Newfront to be exact, will be on IAB Stage on May 3, This will be an opportunity for advertisers to see how they can become part of our culture. Advertisers are finally starting to follow through on aligning with diverse targeted media which means more deals, more deals and more deals! Buying direct with diverse targeted and owned media gives an advertisers an unbelievable reach and frequency with their consumers and especially on free ad supported TV. When advertisers also buy from diverse owned media, Revry is NGLCC Certified and an ANA Diversity Supplier, then they are not only getting the best performance for their budget but also you are investing in building the future of our industry.

The ability to reach diverse, multicultural and LGBTQ audiences will be a recurring theme throughout the year. Especially with LGBTQ audiences since they represent $1.7 trillion of US GDP.

The Newfronts will be more relevant than ever with participants like ourselves representing the diverse LGBTQ community for the first time, along with companies like Estrella, Canela and LATV bringing the power of Hispanic and Latinx consumers.

Ryan Kenney, SVP, Streaming Platform at Magnite felt that OEM-based streaming would play a big role in this year’s upfronts with consumers looking to them for content discovery and ultimately which apps they will add to and keep in their mix while advertisers lean in for the OEM’s valuable ACR data.

Ad-supported streaming will undoubtedly dominate the Upfronts and Newfronts and there are two themes that we believe will encourage a lot of discussions. One is the role of OEMs which heavily impact how audiences access and discover content as well as how ACR data can be leveraged to offer unique advertising value and opportunities.

We can expect to see advertisers asking more questions about how they can creatively engage viewers across various formats within the streaming ecosystem and what data can be layered on top of those buys.

The second topic that will come up in myriad ways is balancing monetization with the user experience which encompasses everything from EPG to navigation to discoverability, and much more. According to research Magnite conducted in the US, 87% of streaming viewers will add a new ad-supported streaming service in 2023. That being said, consumers will gravitate towards seamless ad experiences that enhance the content they want to watch and it’s up to media owners to deliver on that.

Adam Helfgott, CEO at Madhive predicted that brands would be more conservative with their spending this year and less willing to experiment—good news for both Upfronts and Newfronts.

The Upfronts and Newfronts simply serve as a way to secure inventory at scale to keep costs low. We expect macroeconomic headwinds are definitely going to play a role in how advertisers allocate their budgets this year. When the economy is thriving and consumer spending is high, brands are willing to spend in experimental ways… And when it’s not, they don’t. No one wants to be responsible for a failed budget. That’s why Madhive stays focused on efficiency and attribution.

Field Garthwaite, Co-Founder, CEO, IRIS.TV dove into the ways that data was being used for buying, opining that streaming needed more than just household data to be effective while urging the industry to standardize content signals to allow for more contextual buying.

When this year's TV Upfront negotiations go into effect, consumers will be watching more free ad supported streaming than broadcast TV. Negotiations will be prioritized based on the size and scale of partnerships, and incorporate new data standards that enable standardization to address the complexities of buying and measuring streaming at a time when buyers are focused on performance.

Today thousands of FAST channels are available on every smart TV. Smart TV providers have become some of the largest suppliers of quality inventory on the big screen. Data sets that work in TV, aren't scalable in streaming due to the volume of options available to every consumer. Household data only goes so far with multiple people and devices in each home, and data sets that worked in broadcast, like Show and Episode program information, are signals that require manual labor on the buy side to ensure compliance with important upfront terms like Program Restrictions. This doesn't work in streaming. Research showing that 20% of ads in kids content were inappropriate is an unfortunate example of the gaps in streaming data.

The industry is now taking a step forward to standardize content signals so that streaming can be the #1 format for reach and ROI over TV. In the same way data standardization led to scaled buying on identity data, Content ID's like the IRIS_ID will help premium content owners drive more value to advertisers by solving these transparency and performance challenges. Contextual and suitability data segments from trusted data and measurement providers are being used to scale the reach of ad buys, enabling Fortune 500 brands to increase their streaming budgets with confidence.

Dirk Wittenborg, Chairman at Foxxum urged the industry to focus more on real-time results, rather than buying in bulk in advance, while noting a phenomenon he called “recycling” where ad spend is tied to money spent on a particular platform.

Upfronts comes from the old TV model where ad space was limited and results could not be measured. Today we have more ad space than needed and we can measure. If I would spend ad dollars I would do only "Realfronts," test small and increase real-time based on results. Anything else is just ignoring the potential of streaming TV.

I believe that most of the ad dollars we see in streaming are recycled ad spending. Players like Google spend large amounts on ads. In the old days that was an expense only. Today, they tell their agency "Hey guys, here is 100 million dollars. If you want them you need to bring back 100 million to place on YouTube. It will take a while to see who can really acquire real dollars and does not only recycle their own spending.

Our TVREV take is that the distinction between the Upfronts and Newfronts is largely artificial at this point, that Newfronts should be spelled with a lower-case “F”, and that while some advertisers may take a wait-and-see attitude towards buying inventory in advance, others will jump on the opportunity to secure lower priced inventory in advance. That latter group are likely to be advertisers who feel they need to be on TV regardless of the economy.

We also believe that churn is going to play a big role in many advertisers’ decision-making process this year. That includes fear that churn on streaming services may mean that numbers in Q4 are very different than they are in Q2, and fear that an acceleration of cord-cutting may leave many linear TV networks with far fewer viewers six months from now.