Paramount And WB Are Competing For The Same Audience — And That Audience Is Stretched Thin

Competing for identical customers is either an industry’s strongest case for a merger or a bright red flag of vulnerability. On the upside, you consolidate your market power. On the downside, you leave yourself over-leveraged. In the world of modern media, it’s difficult to tell the difference.

M&A Overlap

As you all know, Paramount Skydance is in the process of swallowing up Warner Bros. Discovery. According to Greenlight Analytics as of 2025, 17.7 million U.S. adults across 14.7 million households already subscribe to both Paramount+ and HBO Max. These duals subs are [clears throat]: 185% more likely than the average consumer to be a Millennial, 20% more likely to be Urban, and 15% more likely to be college educated.

On paper, this sounds like the ideal audience consumer from both a content and monetization standpoint. But the real problem is that their attention and wallets are being pulled in multiple directions.

These dual subs are also 168% more likely to subscribe to Hulu and 98% more likely to subscribe to Netflix. They’re multi-streamers with several paid subscriptions taxing their monthly budgets. It’s a voracious and committed entertainment customer base. That’s good. But it’s highly competitive without much financial wiggle room.

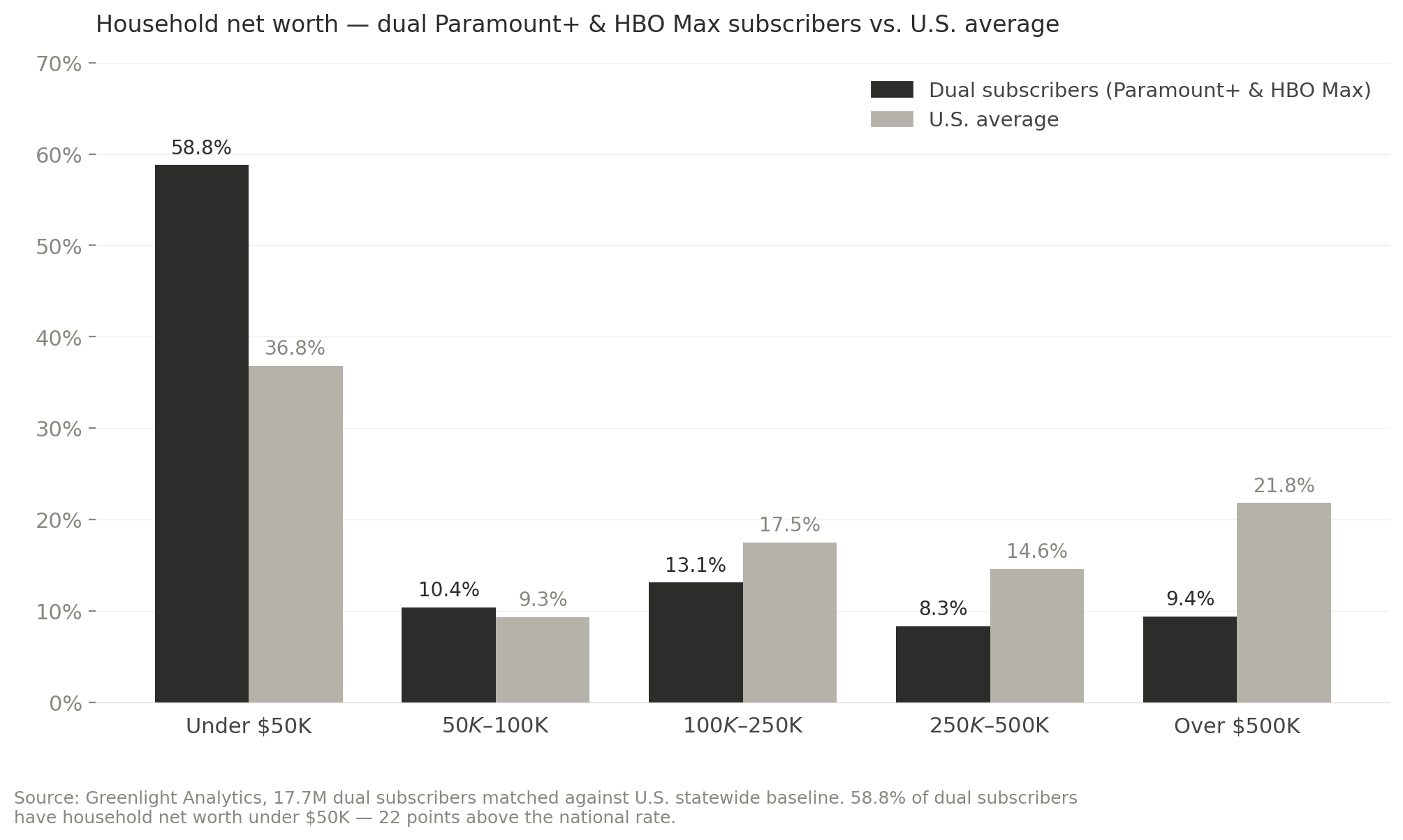

Financial Reality

Roughly 59% of these same HBO Max/Paramount+ users have a household net worth of less than $50,000 vs. 37% nationally, per Greenlight. Only 9% are worth $500,000-plus vs 22% nationally. They are 33% less likely to be homeowners, 28% less likely to prioritize health and wellness spending, and 28% less likely to be donors. (Sorry for all the numbers).

What does this mean for WarnerMount ParaBros?

The combined company’s core domestic audience practices financial discretion and discipline. They are the justifiable manifestation of the “in this economy?!” punchline. Millennials with tangible monetary ceilings that are already spending on streaming may not be the most scalable group. Try spinning that to potential advertisers.

Digital-First

Theatrical still drives flywheels, but this audience already lives on the internet. They are 79% more likely to be streaming-exclusive viewers and 130% more likely to be heavy social media users. Digital natives who largely eschew linear TV.

When they do spend additional money beyond their streaming screens, it’s selective. Far more likely to be IRL experiences such as theme parks and traveling. Theatrical moviegoing diverges from their standard media path.

Warner Bros. + Paramount Pictures

In recent years, the average Theatrical Intent score for films from WB (48%) and Paramount (45%) have consistently fallen in similar ranges. Stability is a virtue in this volatile business. But without growth, Hollywood is simply trying to carve out bigger slices of a shrinking pie.

If your most loyal fans are already stressing financial frugality and are far more likely to stick to streaming only, what’s preventing that 45-48% from winnowing further?

Box Office Optimism

When comparing all films tracked in the first three months of 2026 to the same span in 2025, the tracking data (and box office totals) supports stronger theatrical demand this year.

Interest Among Unaware is up 3.3 percentage points compared to last year. That means a larger share of people are expressing interest in films they didn't know about once presented with the poster/logline. Consider this your persuadable audience: viewers who can be converted to ticket buyers once reached by marketing. This year appears to have more untapped upside thus far.

High Interest is up 2.7 percentage points compared to last year as this year's slate has more titles in the 40%-plus Interest range than 2025. High Interest = A greater number of people are scoring their Interest in a film at 5 or higher out of 7. Coupled with Willingness to Pay (theatrical ticket, VOD transaction or streaming subscription) rising by 1.7 percentage points, an important conclusion can be made. Thus far, people are expressing more interest and a higher share of them are willing to spend money on a title in some form. That translates to more commercial business.

However, Theatrical Intent is only up .2 percentage points compared to last year. Yet given that the 2026 domestic box office is 23.3% ahead of 2025's YTD with more volume, it's safe to say that this year's films are converting Awareness and Interest into Intent at a more efficient clip.

Final Question

Both WB and Paramount boast healthy overall Theatrical Intent trends as they cultivate similar audiences. But those viewers are increasingly stretched thin. They enjoy the content, but prefer to watch it at home where they get the most bang for their buck.

The question isn’t whether the WarnerMount ParaBros merger provides enough scale. Instead, it’s whether intent and behavior are diverging in ways Hollywood can’t account for and whether or not a 2026 theatrical rebound is durable enough to matter.